Once upon a time, Luca Pacioli wrote a math book. It was just a little survey and should have been treated like ordinary books of the time and read and then disappeared into historical archives and forgotten. A few brief chapters on practical mathematics made this one special.

The time was 1494. Columbus had discovered America just two years before. The author was a Franciscan monk.

The time was 1494. Columbus had discovered America just two years before. The author was a Franciscan monk.

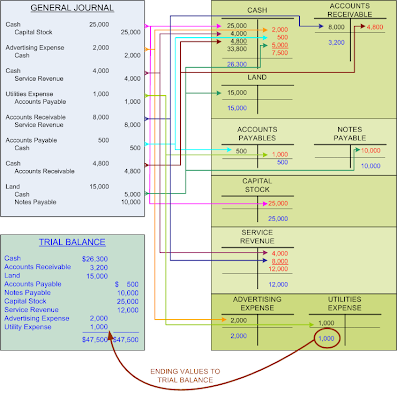

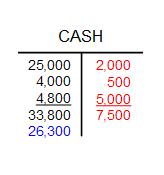

The chapter on practical mathematics addressed mathematics in business. He said that the successful merchant needs three things: sufficient cash or credit, an accounting system that can tell him how he’s doing, and good bookkeeper to operate it. His accounting system consisted of journals and ledgers. It rested on the invention of double-entry bookkeeping. Debits were on the left side because that’s what “debit” meant, “the left”. The numbers on the right were named “credits”.

If everything was done right, then the bookkeeper could do a trial balance (“summa summarium”). Add up all the debits and then add up all the credits, he said. If everything had been done right, the totals should match. If not, “that would indicate a mistake in your Ledger, which mistake you will have to look for diligently with the industry and intelligence God gave you.” He wrote.

Experience

Before computers came along Jack had never got a trial balance right the first time. Many hours were spent looking for the mistakes, though not necessarily with the reverent attitude that Father Pacioli advised!

Double-entry bookkeeping was so simple and met the needs of business so well that it caught on immediately.

In 1850 14 accountants offered services to the public in New York City, 4 in Philadelphia, and 1 in Chicago. The British Isles was the superpower of world commerce. Many enterprises and individuals employed the services of public accountants. Citing the needs of courts to employ public accountants “to aid those Courts in their investigation of matters of accounting” select accountants were titled “Chartered Accountants.” The US equivalent title is “Certified Public Accountant”. These titles are used to this day.

The arrival of the income tax laws were another major event in accounting history. Attorneys naturally thought that since income tax returns were legal documents, they would have exclusive rights to prepare them. Accountants replied that since that the bulk of the work in preparing a return involved accounting calculations, they were more properly accounting work.

The substance of the tasks trumped legal argumentation. US law firms in the 1920’s were slow to incorporate income tax preparations into their business skills. Public accountants saw a new lucrative opportunity and jumped into tax work with both feet. By the time the lawyers challenged the accountants for practicing law without a license, income tax preparation had been so thoroughly identified with accountants that they lost the case.

The Great Depression rocked the integrity of the accounting profession. The British Steamship Company was just one of the large world giants that went bankrupt just after posting large profits. “How could profitable companies go bankrupt?” Investors asked. Court cases showed that the economic reality was that the companies weren’t profitable after all. The profits were the result of bookkeeping tricks. Moreover the reserve funds that were on the books were non-existent.

So far, these events could be chalked up as individuals' fraud (albeit widespread fraud) and handled through the ordinary course of justice. What made the events historic was when the accountants testified in court that the bookkeeping practices were “generally accepted accounting principles” and then proceeded to prove that they were. This was more serious than just individual malfeasance. If the basic rules of accounting gave false information, then something was wrong with the basic rules of accounting.

Worse, followed. Corporate accounting was anything goes. There were no rules, per se. There were just “generally accepted accounting principles”. They were generally accepted because most accountants did certain things. Since accountants were hired by and answered to corporate management, they served the needs of management, not the public. That meant that in practice, the primary function of accounting was to make management look good.

Things had to change. While the profession managed to escape the full New Deal government takeover, rules, standards and legal responsibility had to be shouldered. The American Institute of Certified Public Accountants (AICPA) created their own rule-making body, the Committee on Accounting Procedure. They accepted government licensure. Most importantly, auditing financial statements was limited to CPA’s and they were made personally liable for their audit reports. The new Securities and Exchange Commission (SEC) required audit reports for all publicly traded companies.

With these measures, accountants contributed to restoring public trust in the stock market and the economy during the depression years.

Time passed by. Criticism mounted that the AICPA’s rulemaking was not keeping pace with the needs of the expanding economy. Around 1960 the American Institute of Certified Public Accountants scrapped the Principles Committee and set up the Accounting Principles Board (APB) in 1959. Still the cry for more uniformity and consistency in accounting continued.

In 1973 the Financial Accounting Standards Board (FASB) replaced the APB. It brought two major changes over the previous rules-setting bodies. First it was independent of the AICPA. Second, previous procedural impediments to rule making were overhauled. In short, it was geared to crank out rules – lots of rules.

In the next several decades, it did. And for those accounting areas where it did not want to go, other bodies were set up. There was the Cost Accounting Standards Board and The Government Accounting Standards Board.

In addition to the statements from these Boards, the accountant had to contend with new rules from such sources as Statements of Position, and Accounting and Auditing Guides from the AICPA, and Technical Bulletins and Interpretations from FASB.

By the 1990’s the complaint was “standards overload”. Rule making continued apace.

Ronald Reagan set an historic precedent in 1982 by killing an accounting board (the Cost Accounting Standards Board). The idea that society has enough accounting rules in an area remains a unique event in the history of accounting.

The auditing standards mirrored the accounting standards. Small business was deeply impacted by new auditing requirements. More audit rules meant more audit work and hence more costs to businesses.

In the 1980’s the AICPA announced the Statements on Standards for Accounting and Review Services (SSARS). Henceforth, CPA’s provided three levels of accounting services: 1) Compilation, 2) Reviews and 3) Audits. Auditing: The Expectation Gap covers these. Responding to public pressure, they okayed plain paper “management only” statements in 1998.

Other countries had their own rule-making activities. As the gray areas in accounting came to be covered by rules the flexibility of accountants to accommodate the differing practices of different countries disappeared. What to do?

More rules, of course! The International Accounting Standards Commission promulgated the rules for international accounting. This was set up in Britain just before the turn of the century.

With the corporate scandals directly involving misleading accounting in the early years of the 2000’s, accounting has come back to the days of 1930’s. This time it did not escape direct government oversight.

If everything was done right, then the bookkeeper could do a trial balance (“summa summarium”). Add up all the debits and then add up all the credits, he said. If everything had been done right, the totals should match. If not, “that would indicate a mistake in your Ledger, which mistake you will have to look for diligently with the industry and intelligence God gave you.” He wrote.

Experience

Before computers came along Jack had never got a trial balance right the first time. Many hours were spent looking for the mistakes, though not necessarily with the reverent attitude that Father Pacioli advised!

Double-entry bookkeeping was so simple and met the needs of business so well that it caught on immediately.

In 1850 14 accountants offered services to the public in New York City, 4 in Philadelphia, and 1 in Chicago. The British Isles was the superpower of world commerce. Many enterprises and individuals employed the services of public accountants. Citing the needs of courts to employ public accountants “to aid those Courts in their investigation of matters of accounting” select accountants were titled “Chartered Accountants.” The US equivalent title is “Certified Public Accountant”. These titles are used to this day.

The arrival of the income tax laws were another major event in accounting history. Attorneys naturally thought that since income tax returns were legal documents, they would have exclusive rights to prepare them. Accountants replied that since that the bulk of the work in preparing a return involved accounting calculations, they were more properly accounting work.

The substance of the tasks trumped legal argumentation. US law firms in the 1920’s were slow to incorporate income tax preparations into their business skills. Public accountants saw a new lucrative opportunity and jumped into tax work with both feet. By the time the lawyers challenged the accountants for practicing law without a license, income tax preparation had been so thoroughly identified with accountants that they lost the case.

The Great Depression rocked the integrity of the accounting profession. The British Steamship Company was just one of the large world giants that went bankrupt just after posting large profits. “How could profitable companies go bankrupt?” Investors asked. Court cases showed that the economic reality was that the companies weren’t profitable after all. The profits were the result of bookkeeping tricks. Moreover the reserve funds that were on the books were non-existent.

So far, these events could be chalked up as individuals' fraud (albeit widespread fraud) and handled through the ordinary course of justice. What made the events historic was when the accountants testified in court that the bookkeeping practices were “generally accepted accounting principles” and then proceeded to prove that they were. This was more serious than just individual malfeasance. If the basic rules of accounting gave false information, then something was wrong with the basic rules of accounting.

Worse, followed. Corporate accounting was anything goes. There were no rules, per se. There were just “generally accepted accounting principles”. They were generally accepted because most accountants did certain things. Since accountants were hired by and answered to corporate management, they served the needs of management, not the public. That meant that in practice, the primary function of accounting was to make management look good.

Things had to change. While the profession managed to escape the full New Deal government takeover, rules, standards and legal responsibility had to be shouldered. The American Institute of Certified Public Accountants (AICPA) created their own rule-making body, the Committee on Accounting Procedure. They accepted government licensure. Most importantly, auditing financial statements was limited to CPA’s and they were made personally liable for their audit reports. The new Securities and Exchange Commission (SEC) required audit reports for all publicly traded companies.

With these measures, accountants contributed to restoring public trust in the stock market and the economy during the depression years.

Time passed by. Criticism mounted that the AICPA’s rulemaking was not keeping pace with the needs of the expanding economy. Around 1960 the American Institute of Certified Public Accountants scrapped the Principles Committee and set up the Accounting Principles Board (APB) in 1959. Still the cry for more uniformity and consistency in accounting continued.

In 1973 the Financial Accounting Standards Board (FASB) replaced the APB. It brought two major changes over the previous rules-setting bodies. First it was independent of the AICPA. Second, previous procedural impediments to rule making were overhauled. In short, it was geared to crank out rules – lots of rules.

In the next several decades, it did. And for those accounting areas where it did not want to go, other bodies were set up. There was the Cost Accounting Standards Board and The Government Accounting Standards Board.

In addition to the statements from these Boards, the accountant had to contend with new rules from such sources as Statements of Position, and Accounting and Auditing Guides from the AICPA, and Technical Bulletins and Interpretations from FASB.

By the 1990’s the complaint was “standards overload”. Rule making continued apace.

Ronald Reagan set an historic precedent in 1982 by killing an accounting board (the Cost Accounting Standards Board). The idea that society has enough accounting rules in an area remains a unique event in the history of accounting.

The auditing standards mirrored the accounting standards. Small business was deeply impacted by new auditing requirements. More audit rules meant more audit work and hence more costs to businesses.

In the 1980’s the AICPA announced the Statements on Standards for Accounting and Review Services (SSARS). Henceforth, CPA’s provided three levels of accounting services: 1) Compilation, 2) Reviews and 3) Audits. Auditing: The Expectation Gap covers these. Responding to public pressure, they okayed plain paper “management only” statements in 1998.

Other countries had their own rule-making activities. As the gray areas in accounting came to be covered by rules the flexibility of accountants to accommodate the differing practices of different countries disappeared. What to do?

More rules, of course! The International Accounting Standards Commission promulgated the rules for international accounting. This was set up in Britain just before the turn of the century.

With the corporate scandals directly involving misleading accounting in the early years of the 2000’s, accounting has come back to the days of 1930’s. This time it did not escape direct government oversight.

And they are not living happily ever after.

Source: JACK LE MOINE, CPA

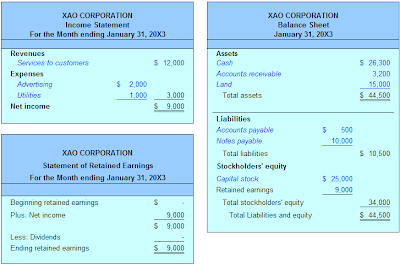

Note that for each date in the above example, the sum of entries under the "Assets" heading is equal to the sum of entries under the "Liabilities + Owner's Equity" heading. In most of these cases, the transaction affected both sides of the accounting equation. However, note that the Sep 25 transaction affected only the asset side with an increase in cash and an equal but opposite decrease in accounts receivable.

Note that for each date in the above example, the sum of entries under the "Assets" heading is equal to the sum of entries under the "Liabilities + Owner's Equity" heading. In most of these cases, the transaction affected both sides of the accounting equation. However, note that the Sep 25 transaction affected only the asset side with an increase in cash and an equal but opposite decrease in accounts receivable. The bike parts are considered to be inventory, which appears as an asset on the balance sheet. The owner's equity is modified according to the difference between revenues and expenses. In this case, the difference is a loss of $175, so the owner's equity has decreased from $7500 at the beginning of the month to $7325 at the end of the month.

The bike parts are considered to be inventory, which appears as an asset on the balance sheet. The owner's equity is modified according to the difference between revenues and expenses. In this case, the difference is a loss of $175, so the owner's equity has decreased from $7500 at the beginning of the month to $7325 at the end of the month.